Special assessments are one of the biggest financial shocks condo owners can face in Florida. They often arrive with little emotional warning, even when the signs were already visible in the building’s finances. For buyers, owners, and investors, the real issue is not only the assessment itself. It is the fact that many people do not understand how or why it happens until the bill is already on the way.

At MAK Realty, we think condo buyers should treat special assessments as a core part of due diligence, not a side issue. In Florida, especially in older or poorly funded buildings, assessments can materially change the cost of ownership. That does not mean every condo is risky. It means every buyer needs a much clearer framework for reading the warning signs, understanding the triggers, and protecting themselves before the problem becomes expensive.

What a Special Assessment Actually Is

A special assessment is a charge imposed by the condo association on unit owners to pay for expenses that the regular budget and reserve funds cannot fully cover. These expenses are usually tied to major repairs, structural work, deferred maintenance, insurance increases, code compliance, safety upgrades, or large capital projects.

This matters because many buyers assume the HOA fee already covers everything. It does not. Monthly dues cover operations and, ideally, some reserve funding. When the association falls short or a major expense appears, owners may be asked to contribute additional money directly. That extra charge is the special assessment.

Why Florida Condo Owners Face Them So Often

Florida condo owners face special assessments more often because the buildings themselves face more pressure. Coastal exposure, humidity, salt air, waterproofing issues, concrete maintenance, aging systems, and stricter repair expectations all create a more demanding environment than many inland markets.

Some buildings also spent years keeping monthly fees too low by underfunding reserves or delaying capital work. That may have felt helpful in the short term, but it often creates a much larger problem later. When major repairs become unavoidable, owners get hit with assessments instead of gradual planning.

The Biggest Warning Sign Is Weak Reserves

If there is one thing buyers should understand, it is this. Weak reserves often lead to special assessments. A building that is not saving enough for future major repairs is much more likely to come back to owners later for extra money.

This is why reserve review matters so much. A building may look beautiful, and the HOA fee may look manageable, but if the reserve account is thin relative to the building’s needs, that lower monthly cost can be deceptive. In many cases, it is simply a delayed bill.

Older Buildings Need More Scrutiny

Age alone does not make a condo risky, but it does make reserve review more important. Roofs, elevators, balconies, facades, plumbing, waterproofing, windows, and structural components all age. If the association has not kept pace, the cost of catching up can be substantial.

That does not mean older buildings should be avoided automatically. Some are very well managed and financially responsible. However, buyers should assume that age increases the importance of reserve strength, maintenance history, engineering review, and pending capital work.

A Low HOA Fee Can Be a Trap

One of the most common buyer mistakes is assuming a lower HOA fee means a better deal. Sometimes it does not. In Florida condos, a surprisingly low fee can mean the association is not saving enough, not maintaining enough, or not preparing for predictable future expenses.

At MAK Realty, we often remind clients that a lower monthly number is only attractive if the building is still healthy behind the scenes. A slightly higher fee in a building with stronger reserves and better planning may be far safer than a lower fee in a building that is quietly heading toward a major assessment.

What Buyers Should Review Before Closing

Before buying a Florida condo, buyers should review the budget, reserve schedule, recent meeting minutes, current assessments, planned capital projects, engineering or structural reports if available, and the association’s general financial health. These documents often reveal whether the building is stable or whether pressure is building below the surface.

The meeting minutes are especially useful because they often show what owners and the board are already discussing. If there is repeated talk of repairs, insurance pressure, deferred maintenance, or financing concerns, that deserves close attention.

Pending Repairs Matter as Much as Existing Assessments

Some buyers focus only on whether an assessment has already been issued. That is too narrow. A building may not yet have a formal assessment, but if major repairs are clearly approaching, the financial risk is still real. In some cases, the assessment simply has not been approved yet.

This is one reason careful reading matters. You are not only looking for what is already charged. You are looking for what is likely coming next. A buyer who ignores pending work can walk into a future obligation that was visible to anyone willing to read the file carefully.

Insurance Pressure Can Trigger Assessments Too

Not every special assessment comes from physical repairs alone. In Florida, insurance costs can also put major strain on condo budgets. If a building’s insurance burden rises sharply and the operating budget cannot absorb it smoothly, owners may feel that pressure through higher fees, special assessments, or both.

This makes condo ownership in Florida more layered than many first time buyers expect. A building may be structurally sound and still face financial pressure from insurance conditions that affect the association’s numbers.

Sellers and Buyers Need to Negotiate This Clearly

If a special assessment already exists during a transaction, buyers and sellers need to clarify exactly who is paying what. This should never be left vague. In some deals, the seller pays before closing. In others, there may be negotiation around credits or responsibility.

A buyer should know not only whether an assessment exists, but also whether another phase may follow later. The current bill is important, but the unfinished project behind it may matter even more.

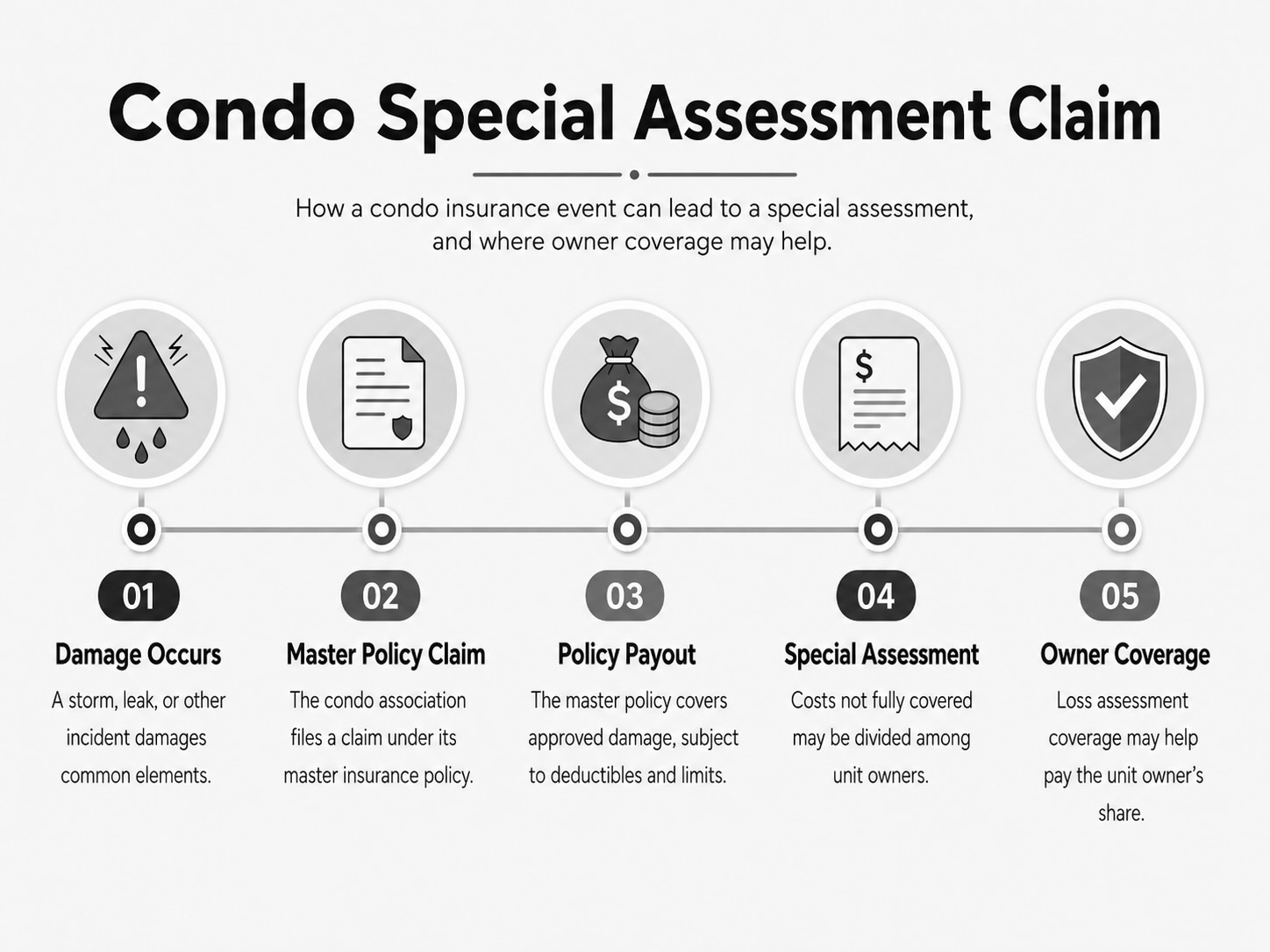

Owner’s Coverage

Your loss assessment coverage may pay your allocated share of the special assessment.

This is one of the most overlooked parts of the conversation. Many owners focus only on the association’s master policy and forget to review their own policy carefully. However, personal condo coverage can sometimes help when a special assessment is passed through to unit owners after a covered loss.

That does not mean every assessment will be covered. Owners need to understand the limits, exclusions, and terms of their own policy. Still, this coverage can matter greatly when the assessment is tied to an insurable event rather than simple deferred maintenance or long term reserve weakness.

How Owners Can Survive an Assessment Better

For current owners, surviving a special assessment starts with understanding the options early. Some assessments can be paid in a lump sum. Others may offer installment terms. Some owners refinance, use savings, or restructure other assets to absorb the cost. The right move depends on the size of the assessment and the owner’s broader financial position.

The worst approach is usually avoidance. Once an assessment is on the table, the smartest move is to understand the timeline, confirm the payment structure, and evaluate how it affects both short term cash flow and long term ownership plans.

When an Assessment Does Not Mean You Should Panic

Not every special assessment means the building is a disaster. Sometimes a well run association raises money for a necessary repair precisely because it is acting responsibly. The key question is not simply whether an assessment exists. It is why it exists, how the board is handling it, and whether the repair strengthens the building’s long term health.

This is where context matters. A one time assessment tied to clear capital work in a strong building may be very different from repeated assessments in a property with weak reserves, poor planning, and ongoing deferred maintenance.

Special Assessments Affect Resale Too

Assessments can affect resale in two ways. First, they directly affect affordability because buyers have to absorb the extra cost or the fear of further charges. Second, they can change how a building is perceived in the market. A property with repeated financial surprises may lose appeal relative to better managed competitors.

That is why special assessments are not just an ownership issue. They are also a resale and marketability issue. Buyers in Florida increasingly pay attention to building health, and that attention can shape how well a condo performs later.

The Smartest Protection Is Buying the Right Building

The best survival guide is really a prevention guide. The strongest protection against special assessment pain is choosing the right building before you buy. A condo with healthier reserves, stronger management, better maintenance history, and more responsible planning gives buyers much more safety than one that simply looks good on the surface.

At MAK Realty, we help buyers look beyond the unit and evaluate the financial life of the building itself. In Florida, that is not optional. It is one of the clearest ways to avoid expensive surprises and make a much stronger condo decision.

What This Means for Florida Condo Buyers Now

Florida condo buyers should assume that building quality is financial quality. A condo is not just a residence. It is also a shared financial system. If that system is strong, ownership can feel stable and predictable. If it is weak, the cost can rise sharply through assessments, higher fees, and repair driven stress.

The smartest buyers do not just ask whether the condo is beautiful. They ask whether the building is prepared. That is the question that usually matters most once the closing is behind you.

For a tailored shortlist and next step guidance, connect with MAK Realty.